March 27, 2026 · Yalid Rahman, Mainak Ghosh

Tokenizing Structured Products: The On-Chain Evolution

Ironlight's on-chain infrastructure tokenizes structured products like CMBS and CLOs, replacing manual waterfall processing with smart contracts that automate lifecycle payments, reduce costs, and enable secondary trading.

Structured products — from Commercial Mortgage-Backed Securities (CMBS) and Collateralized Loan Obligations (CLOs) to Asset-Backed Securities (ABS) — form the backbone of institutional fixed-income markets, channeling capital into real estate, corporate lending, and consumer credit at scale. In the U.S. alone, the CMBS market totals approximately $1.7 to $1.8 trillion in outstanding debt, while the broader structured finance universe exceeds $12 trillion. Major banks such as JPMorgan, Wells Fargo, and Goldman Sachs sit at the center of these securitizations, orchestrating complex waterfalls that allocate cash flows across dozens of tranches with differing risk profiles. Yet the infrastructure underpinning these markets remains stubbornly manual: deal settlement stretches across days, reporting lags behind reality, and investors often lack real-time visibility into the very cash flows they're entitled to. In 2025, with over $150 billion in CMBS loans maturing and office property delinquencies nearing 10.6%, the cost of that opacity is becoming harder to ignore.

At Ironlight, we've built on-chain infrastructure for structured products that tokenizes the entire lifecycle of a structured product, from issuance, to distributions, to redemptions. The system even handles market disruptions. In this post, we'll unpack both why bringing structured products on-chain matters and how we made it work.

But first, what exactly is a structured product? From Investopedia, “structured products are prepackaged investments that typically combine assets linked to interest rates with one or more derivatives.” An example would be a reverse convertible note linked to Salesforce stock: It pays an above-market coupon rate but carries the risk that if CRM stock drops below a set "knock-in" level, the investor receives CRM shares instead of cash at the end of the term. It is designed for investors who want to earn a high yield and believe that the underlying instrument will trade above the knock-in level for the term of the product.

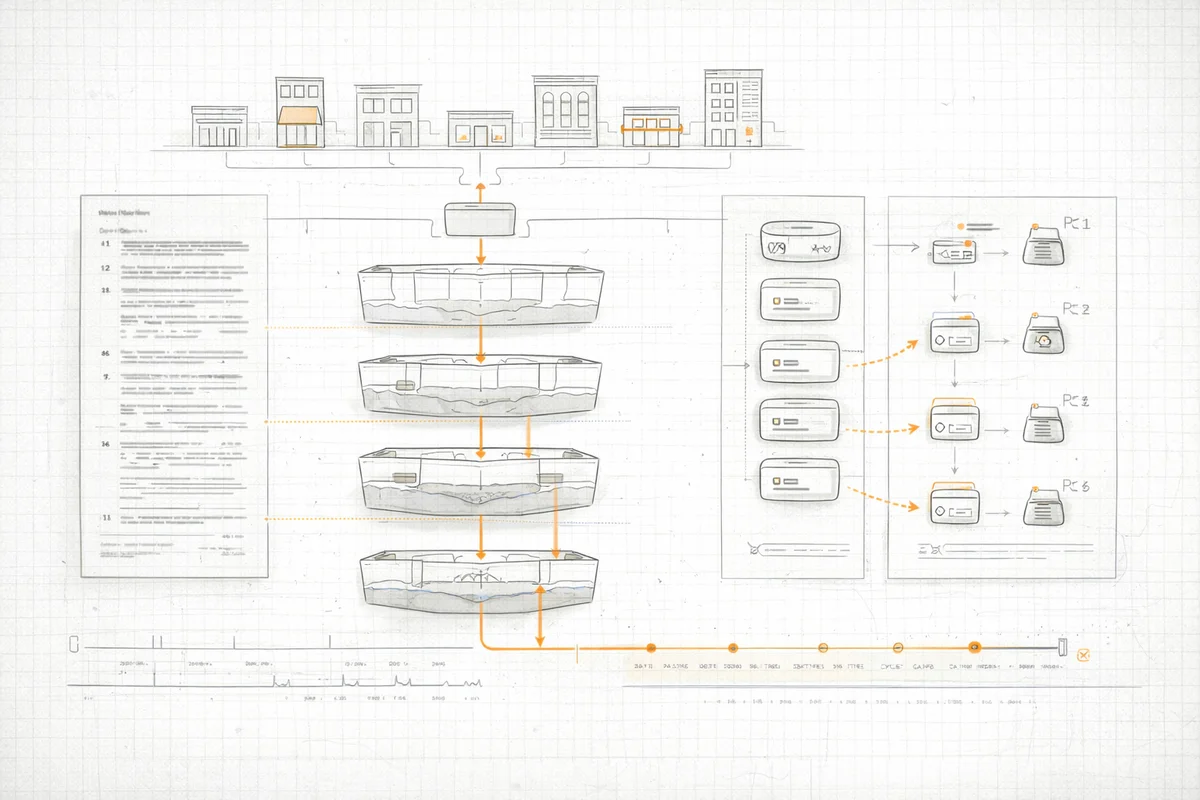

To learn why tokenizing this asset class is important, it helps to understand how operationally complex structured product cash flows actually are. Consider a CMBS as a representative example. When a commercial borrower makes a monthly mortgage payment, those funds don't flow directly to investors. Instead, they pass through a chain of intermediaries — primary servicers, master servicers, trustees, and certificate administrators, each performing their own reconciliation, compliance checks, and reporting before forwarding the funds along. Master servicers collect and aggregate payments from borrowers, reconcile them against loan-level records, and prepare remittance reports. These are then passed to the trustee, who validates the data, applies the waterfall logic dictated by a Pooling and Servicing Agreement (often 400–500+ pages of legal documentation), calculates each tranche's allocation, and finally instructs the paying agent to distribute funds. In many cases, payments between these parties still move via scheduled wire transfers on fixed monthly cycles, with reconciliation performed manually across spreadsheets, PDFs, and legacy servicing platforms. The result: several days (or sometimes even weeks) of delay between the moment a borrower's payment is received and the moment an investor sees cash in their account. This leads to millions in idle capital and lost float at any given time.

The lack of secondary trading compounds this problem. Structured products are inherently bespoke as each deal and issuer carries its own collateral pool, waterfall logic and legal documentation, making comparability across deals difficult and price discovery slow. For many structured products, there is effectively no liquid secondary market. Investors who want to exit an illiquid position have to face weeks of negotiation and manual document review just to close a trade. Often they have no option but to sell the note back to the issuer at a heavy discount.

Here's why tokenizing structured products makes sense:

-

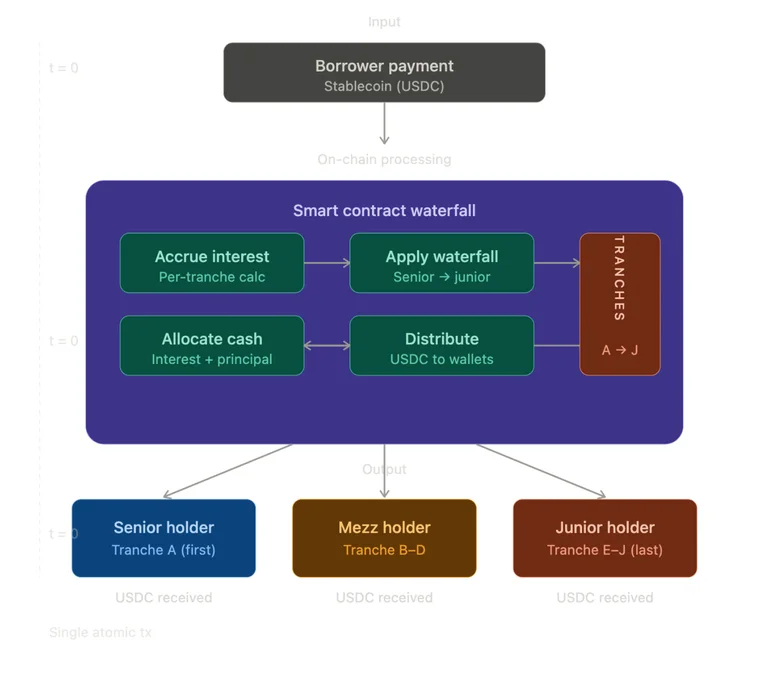

Automated and real-time lifecycle payments. Instead of waiting for a mortgage servicer and trustee to reconcile payments and work out the waterfall manually, a smart contract executes the entire waterfall whenever funds arrive. In our testing on tokenized CMBS products, we’ve been able to distribute proceeds directly to investor wallets within a minute of the payment.

Of course, tokenization also opens up the possibility of product innovations. Due to the faster lifecycle processing, it is now possible to think about products that have daily payouts or even ‘streaming’ products that pay out a cash flow continuously.

-

Operational efficiency and cost savings. The servicing ecosystem of servicers, trustees, and legal teams independently maintain records of the same transaction. This was partly by design (maker-checker processes designed to catch errors or wrongdoing) and partly a historical legacy as firms just do not like sharing data with each other. A blockchain is an elegant design solution to this entire issue, creating a single source of truth, world-readable and auditable by anyone at any time while still maintaining anonymity of the investors. Eventually, we see a world where much of this servicing ecosystem is replaced by smart contracts.

This has the effect of reducing or eliminating the fees that keep these products limited to ultra-high net worth or institutional investors. Costs like legal review for each bespoke contract and fees for trustees, custodians and payment agents are the main barriers that keep the minimum ticket size for these products as high as $250k on the low end. We could soon be looking at a world where a $10k minimum is viable.

-

Standardization leading to secondary trading. The first step to tokenize a product is to transform the prospectus of the note into a smart contract, standardizing each clause of the (legal) contract into (smart) contract functions. This has the effect of making terms comparable across issuances, enabling price discovery and laying the groundwork for on-chain secondary markets. Ironlight’s unique open-access model can aggregate demand across multiple broker-dealers and RIAs, potentially creating a much larger pool of liquidity than any single prime broker or issuer can create today.

-

Collateral mobility in DeFi. Once a structured note exists as a token, it can serve as collateral, thus unlocking a new layer of utility. The token can be deposited into a decentralized finance (DeFi) protocol and used to borrow against, providing access to liquidity and leverage without requiring the position to be sold.

At Ironlight, we first developed digital twins of existing CMBS and structured product deals. For the CMBS, each tranche is a distinct ERC-3643 token. An investor holds the tokens in proportion to their ownership of each tranche. The ERC-3643 security token standard allows us to enforce securities laws on-chain, giving us the ability to limit holders to KYC’d accredited holders only. A central deal contract contains the full payment waterfall. This contract monitors incoming cash flows as a mix of principal and interest, calculates interest to the required precision and automatically distributes it to the holders.

Now, the distribution required another innovation. Most crypto yield tokens either rebase (increasing your balance) or accumulate (appreciating in price). In either case, the yield is received in units of the token itself (a sort of payment-in-kind). However, we believe investors prefer to receive their yields in their wallets without taking any manual actions. Therefore, we took a new approach: our tokens distribute, meaning yield is delivered directly to holders' wallets as stablecoins the moment cash is received, with no manual action required. If tokenized money market funds are used instead, the funds begin accruing additional interest immediately. This design mirrors how traditional fixed-income distributions have always worked, helping TradFi investors onboard without changing their models and processes.

Similarly, for structured products that have periodic distributions, the smart contract receives funds from the issuer and distributes them to the token holders in real time. If distributions are contingent (usually upon the price of an underlying asset), a price feed from an oracle can be used. The contracts can operate either fully automatically, in which case no manual intervention is needed, or they can have wallets that play the role of calculation agents and payment agents, allowing a level of manual control and oversight before the distributions are made. We believe that, as the industry gains more confidence in the operation of these contracts, they will overwhelmingly shift to running fully automatically.

We believe this approach has value for everyone involved in the structured product ecosystem: issuers looking to streamline their deals, investors seeking better liquidity and clarity, servicers who want to automate manual tasks, and even regulators who want real-time visibility into payment flows. Ironlight is partnering with multiple players to bring tokenization to this space. If you’re in this world—as a structurer, buyer, seller, or servicer—we’d love to show you how it works. The future of structured finance is already here. We invite you to build it with us.